We'll start this week's newsletter by looking backward at data, then forward, then at the theme of inflation that has emerged in recent weeks, and close with a few words about the minimum wage.

Gross Domestic Product for the fourth quarter of 2020 was released on Thu Jan 28, and it showed +4.0 growth (annualized rate). Regular readers will know that I have been tracking the running estimate known as GDPNow produced by the Federal Reserve Bank of Atlanta. It had been predicting GDP growth more like 7.2%, so +4 was disappointing. The Yahoo! News report linked above quotes the official Bureau of Economic Analysis press release as saying, "The increase in fourth quarter GDP reflected both the continued economic recovery from the sharp declines earlier in the year and the ongoing impact of the COVID-19 pandemic, including new restrictions and closures that took effect in some areas of the United States."

A growth rate of 4% is above what we normally think of as the long-run sustainable rate, but starting from spring 2020's COVID-depressed levels—even after Q3's huge surge of +33.4%—there's more room to grow than what we saw in Oct-Dec. All the observers I follow agree that the economy is poised for a big acceleration of growth in the course of 2021, as soon as sufficient numbers of people feel safe through vaccinations. [See below in the FORWARD section extended evidence in support of this claim.]

(By the way, in spite of what I see Martha Radditz trying to tell us on today's ABC Stephanopolous This Week Sundayshow, West Virginia is not the only place where vaccinations are proceeding without drama or turmoil: my mother in Montana and my bro & sis-in-law in Arizona all got their first jabs this past week, after placing a single, simple phone call for an appointment, showing up, and that's all there was to it.) We're now at 1.3 million vaccinations daily, which would be about 9 million or about 2.7% of the population each week. But it's not "each week," since the daily number is rising steadily. Even a week ago, the 1.3m figure was more like 1.1m, if I remember what I heard at the time. So the 1.3m figure is both the highest ever, and the lowest that it will be for the rest of the first half of the year, as production and distribution numbers improve constantly. With Johnson & Johnson's vast production capacity about to be added to the mix (and the advantage of their shot being a single-jabber), we'll be adding 3, 4, maybe 5% of the population to the immunity pool every week in the spring. By one or another of the summer months, I expect that we'll be at the "there will be orgies" stage. I'm with Andrew Sullivan: "… we will travel in unprecedented numbers; and after a grim year of withdrawal, fear, anxiety, and solitude, we will become human again."

If I'm right about all of the above, then a lot of what I have been doing in these newsletters is beside the point. Whether housing starts or consumer confidence or factory orders rises a little more or less than expected during one of the months of this winter is largely stochastic (fancy econ-speak for "random") noise that has little to no predictive power over what will happen the next month, let alone in June or August. What does affect our rate of improvement in June or August, aside from the vaccinations, is a whole lot of exogenous (fancy econ-speak for "outside") shocks emanating from D.C. Last weekend I mentioned the 30 executive orders from the Biden White House; since then there have been 10 more. It's possible to find some reporting on the basic facts of what they are, but much harder to find anyone scrutinizing what they really mean and the ways they might screw us up.

Looking for inciteful analysis, I tried this weekend's New Yorker Radio Hour on NPR, and found instead only a 4-year-old repeat of someone criticizing the ex-president's Christianity for the majority of the hour. Because, you know, there's not much else going on worth the New Yorker journalism team spending any energy on. Most of the rest of the time was a boring interview with a not-very-good singer-songwriter I had never heard of. There was also a puff piece praising the new president's Christianity. One sample: "People on the left are now looking to Biden to bring his religion into the mix." My, how things have changed since the '80s when a major national obsession was the fear of religious people "imposing their morality" on others. Now, it seems, almost all we do in our diminishing public square is root out the immorality of other people's wrong-think.

But I digress from my main point, which was that I will probably redirect these newsletters away from the weekly and monthly indicators that I have just shown to be "beside the point," and toward some attempt to fill the void of scrutiny and inciteful analysis that I have just noted.

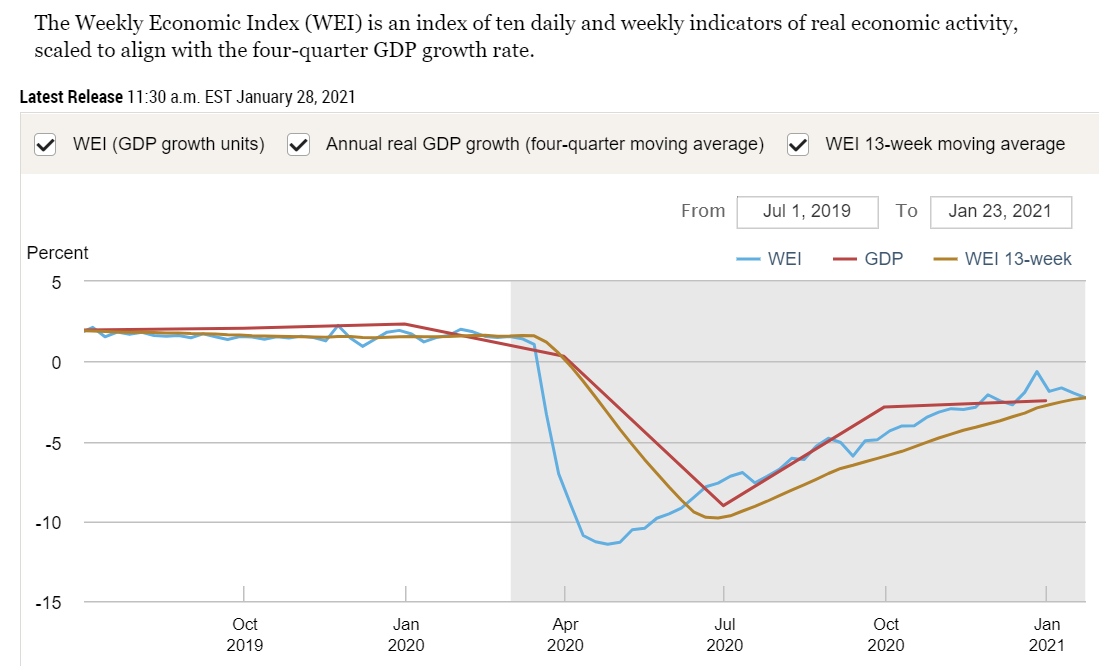

Even so, a little more about the GDP numbers. I was saying in the short paragraph near the top that we still have room to grow. That is shown in the graph below from the Federal Reserve Bank of New York's Weekly Economic Index. Generally, I focus on the right end of the weekly blue line. What we see there is a set of 10 daily and weekly indicators curated by the NY Fed having shown no net progress since Thanksgiving. The latest reading shows us being -2.28% below the level of one year ago. Since we ordinarily want and expect to be growing at a positive +2 or more percent (as seen in the July '19 - Feb '20 left half of all 3 lines), the -2.28 number means we are about 4.5% below where we want to be in terms of overall economic health. (GDP measures the inflation-adjusted value of all marketable final goods and services produced.)

But what I thought was interesting about this week's graph was not so much the right-hand tail of the weekly blue line but rather that addition of a new segment of the quarterly red line for GDP itself. It's just about flat (actually up from -2.85 to -2.46), which reinforces that Thursday's headline of 4.0% Q4 growth was just more than enough to tread water. That is, the economy had grown by about as much from Q3 to Q4 last year, so our improvement from Q3 to Q4 this year still leaves us near the same deficit of about 4.5% below par (with par being the good ol' pre-COVID days through Feb '20).

GDP looks backward by one to three months—back to the Oct - Dec interval in this case. We get a little more useful info by looking back just one month with the detail about personal income and consumption, which always trails the GDP data release by one day. So on Fri Jan 29 we learned that "Personal income rises more, consumer spending falls less than expected in December," according to a paywalled article's headline on SeekingAlpha.com. More accessible details are available here. In short, the rise in personal income was +0.6% in December (un-annualized). Even after accounting for a downward revision to Nov, the net change was about 3 ticks better than a survey of economists had been expecting. The fall in consumer spending was -0.2%, which was better than expectations, or about on par after accounting for revisions. So, not a very dramatic report, but mildly positive.

The same report includes a measure of inflation known as the price index for core personal consumption expenditures (PCE), which is the measure of inflation most followed and targeted by the Federal Reserve when they set monetary policy with interest rates and the money supply. It varies in theory, if not very much recently in magnitude, from the famous Consumer Price Index (CPI) that is used by the media and general population to measure inflation. (CPI is also used by the Social Security Administration to set Cost of Living Adjustment raises to benefit checks.) This core PCE inflation index "ticked up to 1.5 percent in December from 1.4 percent in November," to quote from the same Nasdaq article linked above.

FORWARD

Such an uptick is so small as to be 'stochastic,' but I mention it here because it does give a modicum of evidence toward an emerging thesis of mine: we are seeing inflation accelerate. Although I'm 30 years out from being a professional macroeconomic/econometric modeler and forecaster, and I have no access to any sophisticated statistical tools, I do believe that I've noticed enough bits of evidence to support a case for accelerating inflation. I've convinced myself, at least, that it is already happening and is likely to continue this year.

Not everyone agrees, starting with the person whose opinion matter more than any other—Federal Reserve Board Chairman Jerome Powell. Before turning back to inflation, I want get to the FORWARD section of this newsletter by quoting from Powell's unscripted comments this week about the 2021 outlook for the economy and monetary policy. (I have not found the original primary source, so I excerpt from Prof. Tim Duy's partial transcript included in this blog post; emphasis added.)

there’s good evidence to support a stronger economy in the second half of this year. In fact, if you look as we do at a range of private forecasters, what was their forecasting in December and what’s their forecast now, right across the board: much higher forecast for 2021 growth because of the on going rollout of the vaccine and CRA act getting done. There is a positive case there, but that — think of that as the sort of base case is a strong economy in the second half of the year. … There are considerable risks of economic outlook nonetheless that is a more positive outlook and that’s how I would parse that for you.

The other thing, even conditional on that, when we say the wave in the south and west, the wave of cases this summer, I think intuitively having seen what happened in March and April, we expected there to be a significant hit to economic activity and people kind of just got on with their lives and dealt with it. It had a much smaller effect on economic activity than we expected. Then comes the fall wave which is just so much larger, very large wave as was very much forecast people going indoors, the weather all that. Even there look at the December jobs report. So big job losses and, you know, that part of the service sector, I mentioned 400,000 jobs [lost] in bars and restaurants, another hundred thousand in similar kinds of activities. If you look elsewhere, it’s not having an effect. You know, purchasing manager index, incentive index on areas of the economy not really directly exposed to the pandemic in their economic activity, they’re doing okay. They are. Housing is a great example. You know, the way the housing industry worked when you buy a house there was a lot of in person contact.

All of this, from the Chairman of the Federal Reserve, is a very close paraphrase of my main point in the Jan 18 No-BAH-DI-NOZ newsletter where I wrote, with bolded emphasis and in the opening summary:

Evidence indicates that the core of the economy is intact, is growing where and when it can (but being slammed by COVID in [only] the sectors where it makes sense that it would be), and is ready to resume full strength when COVID pressures relent.

INFLATION

Here is what Chairman Powell had to say about inflation, as introduced in the same Prof. Tim Duy blog:

Moreover, Powell pushed back hard on inflation concerns. He emphasized that the Fed would not be fooled into an inflationary scare attributable to either base effects or the initial phase of a rebound. Importantly, he very carefully explained that the economy has been locked into a disinflationary dynamic that will not be easy to change. For example:

…it helps to look back at the inflation dynamics that the United States has had for some decades and notice that there has been, you know, significant disinflationary pressure for some time for a couple of decades. Inflation has averaged also [less] than two percent for a quarter of a century and the inflation dynamics from the flat Phillips curve and low persistence of inflation changes over time. It evolves constantly over time but don’t change rapidly. It’s very unlikely anything we see now would result in troubling inflation. Of course if we did get sustained inflation level that was uncomfortable, we have tools for that. It’s far harder to deal with too low inflation.

All month in these newsletters I have been noticing and pointing out evidence to the contrary. Let's review.

From Jan 3:

Morgan Stanley simultaneously released a 15-minute podcast explaining their forecast. The emphasis there is that Morgan Stanley is more optimistic than are many other forecasters. … They are also somewhat outliers in calling for an acceleration of inflation, and I mean to write some time soon about why I agree with that.

From Jan 10:

I quoted from www.nar.realtor/pending-home-sales where NAR's chief economist spoke of "fast-rising home prices. … It is important to keep in mind that the current sales and prices are far stronger than a year ago."

American manufacturers have gotten better at safeguarding their factory floors and containing infections of Covid-19 in their workforces. Despite the progress, they are still struggling to find enough people to staff their plants. The worker shortages are choking supply chains and delaying delivery of everything from car parts to candles just as demand is picking up… A generator maker is so backed up on orders due to absenteeism that it has raised starting pay 25%.

Also that week I cited the Federal Reserve Bank of New York's monthly Survey of Consumer Expectations, which found (small) increases in inflation expectations, both 1 year and 3 years ahead.

From last week, Jan 24:

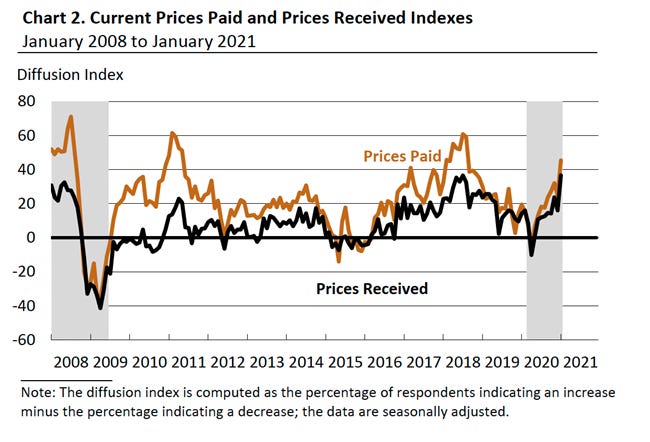

I excerpted this heading, paragraph, and chart from the Philadelphia branch of the Federal Reserve about their monthly Business Manufacturing Outlook Survey:

Price Indicators Increase This Month

Price increases were more widely reported this month. The prices paid diffusion index increased 21 points to 45.4 (see Chart 2). Over 47 percent of the firms reported increases in input prices, while only 2 percent reported decreases. The current prices received index, reflecting manufacturers’ own prices, also increased 21 points to 36.6. Over 38 percent of the firms reported increases in prices of their own manufactured goods, while 2 percent reported declines.

Here's a report that I missed last week:

… from Jan 22 about the IHS Markit's purchasing managers' index (PMI) of economic activity. Their press release begins by spelling out a bunch of good news, up to the fifth paragraph where we see the effects of that good news—cost-push inflation even before we add to it post-COVID's pent-up demand coming later this year (emphasis added):

Private sector businesses in the U.S. indicated a strong start to 2021, as output and new orders rose further. Rates of expansion in business activity accelerated at manufacturers and service providers, with goods producers registering the sharpest upturn in output since August 2014.

Adjusted for seasonal factors, the IHS Markit Flash U.S. Composite PMI Output Index posted 58.0 in January, up from 55.3 in December. The private sector seemed to regain growth momentum at the start of 2021, as the pace of increase quickened to the second-fastest since March 2015.

At the same time, private sector businesses signalled another monthly increase in new business. That said, the overall rate of growth eased from that seen in December, as service providers indicated a slower expansion in new orders following a rise in virus cases and greater restrictions on business operations.

Nonetheless, the upturn among manufacturers accelerated and was the steepest since September 2014. Encouragingly, private sector firms signalled a renewed and solid rise in new export orders during January.

Meanwhile, inflationary pressures intensified as supplier delays and shortages pushed input prices higher. The rate of input cost inflation was the fastest on record (since October 2009), as soaring transportation and PPE costs were also noted. A number of firms were able to partially pass-on greater cost burdens, however, as the pace of charge inflation quickened to a steep rate. The impact was less marked in the service sector as firms sought to boost sales, but manufacturers registered the sharpest rise in selling prices since July 2008.

Then, this week I add:

… the following headlines, which I collected while not even looking for them in the course of being overly busy with my day job [8 more deadlines to be met Feb 1-5]. Taken all together, in combination with the citations above from Jan 3 - Jan 24, the evidence for inflation already having arrived seems to me fairly overwhelming. Here they are in raw form so you can get the gist from the headlines built into the URLs:

About that last headline, stating that a higher minimum wage would confer some benefits, I add these two paragraphs of commentary:

Yes, it will benefit some people, and what the headline neglects to add is that it will inevitably harm others. Some people will get a raise, and some will see their jobs lost and incomes cut to zero. In that sense, a minimum wage hike increases income inequality within the low-paid tier. If you don't believe that a raised minimum wage kills jobs, why stop at $15/hour? As sure as night follows day, within the same hour as the federal min-wage being raise to $15, we'll hear in chorus the truism that "you can't raise a family on fifteen dollars an hour," and the campaign for a $20 or $25 min-wage will be underway. So I ask again: if a higher min-wage comes can be done without loss of jobs, why not just set it at $50/hour? Or $150? Or any arbitrary number we decide on?

More broadly, my response to the claim in the final headline is this: Of course any policy choice will—one certainly hopes—benefit some faction. But it's almost axiomatic that the same policy will harm others. So to come out with a claim like the one in the headline is merely to say that the idea is not purely a destructive act, with no offsetting gains to anyone. That's such a low bar as to be meaningless, if what we're trying to be engaged in is a rational discussion (rather than, say, brute-force politics). The more important matter is whether the gains to some are greater than the costs to others, and if not, whether you can make a case that it is good policy to enact the policy even though the costs outweigh the gains. That's the sort of intellectual habit that a careful study of economics, particularly a good course in microeconomics, leads people to internalize. The absence of such training leads people to see a policy that claims a benefit somewhere along the line and respond in knee-jerk fashion: Let's do it! The "at any cost" or "by any means necessary" reaction is the instinct of totalitarianism; the study of economics is the antidote for that frightful tendency.