Consumers, Economists, and Congressional Budget Office All Expect Stronger Economy

…Prompting fears by many of us that inflation is the next risk

The first lesson of economics is scarcity: there is never enough of anything to fully satisfy all those who want it. The first lesson of politics is to disregard the first lesson of economics.

-T. Sowell

Much of this newsletter consists of some further comments, links, and excerpts about expectations of accelerating inflation, but I'll start with a rundown of several high-level views of where the whole economy is and where it is headed.

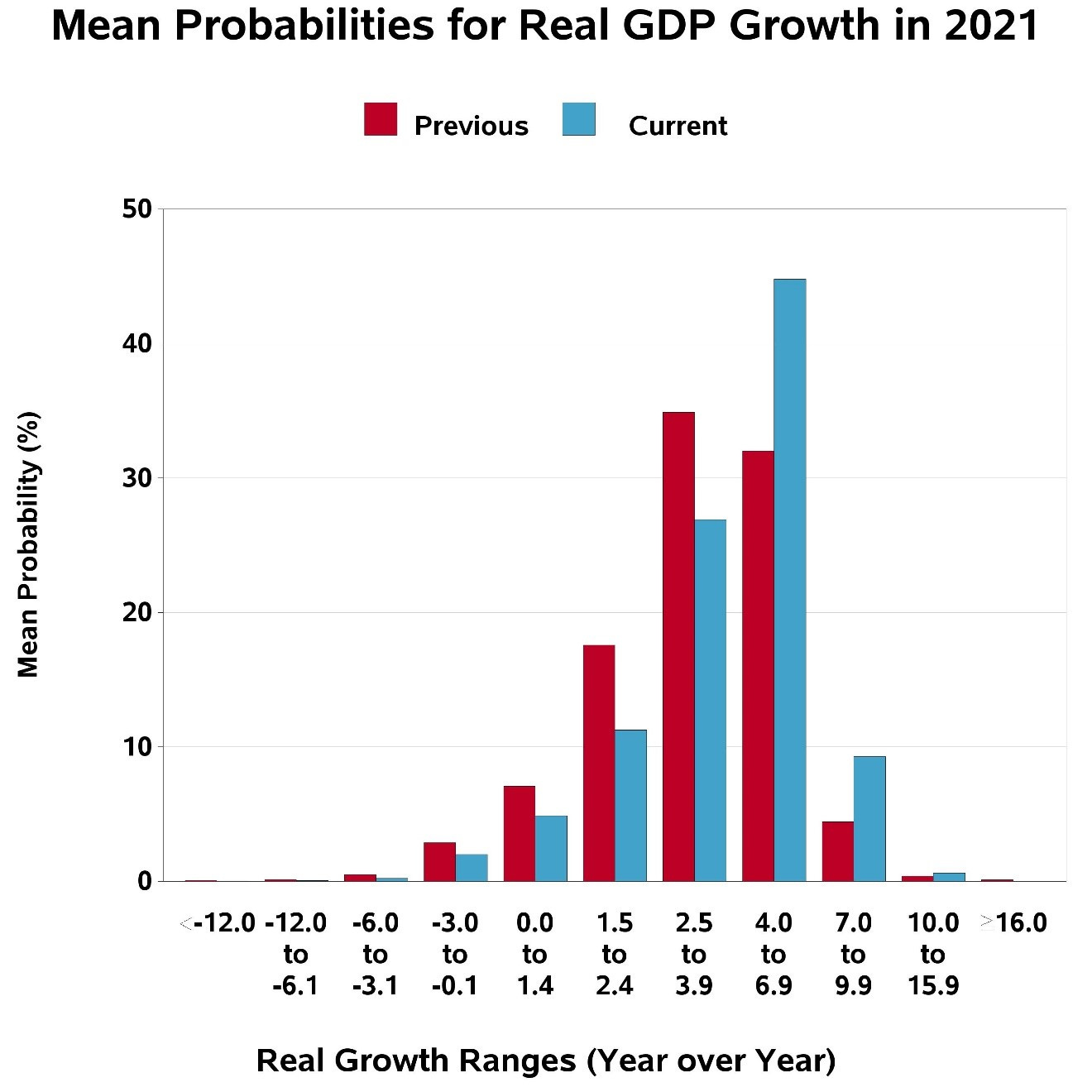

The Philadelphia branch of the Federal Reserve System conducts a quarterly Survey of Professional Forecasters and has prepared a nicely informative press release, which begins "The outlook for the U.S. economy over the next three years looks stronger now than it did three months ago." I'll add that the outlook as of 3 or 4 months ago was already massively improved from earlier in 2020, which formed the basis for maybe my best effort in this newsletter project.

Quoting more from the press release:

the forecasters expect real GDP to grow at an annual rate of 4.5 percent in 2021 and 3.7 percent in 2022. The projections for 2021 and 2022 are up from 4.0 percent and 3.0 percent, respectively, in the last survey.

A brighter outlook for the unemployment rate accompanies the outlook for growth. The forecasters predict unemployment will decrease from a projected 6.3 percent this quarter to 5.1 percent in the first quarter of 2022. On an annual-average basis, the panelists predict the unemployment rate will decline from a projected 5.9 percent in 2021 to 4.0 percent in 2024. The annual-average projections for 2021, 2022, and 2023 are 0.4 percentage point below those of the last survey.

They prepared this chart showing how the expectations for this year's total economic growth rate have shifted from the 2 to 4 or 5% range to the 3+ to 6 or 7% range. The biggest change, an increase, came in those expecting 4-7%, which is now the most common guesspectation.

[the chart is hot-linked]

The Philly Fed survey respondents also agree with me [see below] that inflation will accelerate from here. The actual, current statistics were released Wednesday by the Bureau of Labor Statistics, showing that the Consumer Price Index (CPI) had risen 1.4% from one year ago. I've you're earning less than that in a savings account or CD, or if your annual raise is less than that, you're going backward. The surveyed forecasters see 2.5% for the Jan-March quarter, up from 2.0% in their last guess three months ago. Inflation functions as a tax on cash balances. It pushes savers into riskier investments in an attempt to keep up. Those investments may be inappropriate for people who really need safety, and may further imbalance the already (arguably) crazy valuations in stocks, cryptos, real estate, etc.

Meanwhile, the New York branch of the Fed came out Monday 8 Feb with their monthly Survey of Consumer Expectations, which I have taken time to analyze in some depth one month ago and in some previous months.

The summary paragraph of the above-linked press release is here:

The Federal Reserve Bank of New York's Center for Microeconomic Data released the January 2021 Survey of Consumer Expectations, which shows that households' year-ahead spending growth expectations rose to 4.2%, the highest level recorded in more than 5 years. In contrast, earnings growth expectations have remained flat for the sixth consecutive month. Labor market expectations continued to improve with higher expectations about job security and job finding. Home price expectations rose again in January to reach their highest level since May 2014. Median inflation expectations were flat at both the short and medium-term horizons, while inflation uncertainty and inflation disagreement remain elevated compared to pre-COVID-19.

That paragraph highlights that "earnings growth expectations have remained flat," but concerning a very similar-sounding concept, they say this: "The median expected growth in household income increased by 0.2 percentage points to 2.4% in January, the highest level since February of last year." The easiest explanation would be that 'earnings' specifically means from earned income from paychecks, while the concept of 'income' includes that plus unearned income including transfer payments—i.e., Free Money checks in the mail. But I have never learned for sure how the New York Fed defines and distinguishes these terms.

Other than the ambiguity about earnings and income, the rest of the report was reassuringly positive. There's more than what made it into the intro paragraph:

The mean perceived probability of losing one's job in the next 12 months decreased for the third consecutive month from 15.0% in December to 13.6% in January, the lowest reading since September 2019. The decrease was more pronounced among respondents with lower education (no more than a high school degree) and lower household income (less than $50,000).

Perceptions about households' current financial situations compared to a year ago improved slightly in January, with fewer respondents reporting that credit is harder to obtain. Respondents were also slightly more optimistic about their households' financial situations in the year ahead with more respondents expecting their financial situation to improve a year from now.

The median expectation regarding a year-ahead change in taxes (at current income level) increased for the third consecutive month to 4.4% in January from 3.3% in December. This is the highest level since September 2013.

On Feb 1 the nonpartisan Congressional Budget Office (CBO) released their first major official forecast since June 1, and it said broadly the same optimistic things. See in the screenshot of headlines from that day that the CBO's outlook is highly positive. Even so, if you're a media outlet looking to find a negative way to spin it, the Washington Post proves that it can be done.

The last of those headlines, the one from CNBC, is linked here, but I'm not going to go through all the text and provide analysis because I'm at about one-third speed today after getting my second singles (Shingrix) vaccination yesterday.

Two weeks ago I closed with a mini-editorial about raising the minimum wage. Speaking of the CBO, they have run the numbers—that's what they're famous for doing—generating this headline from last Monday.

"Raising minimum wage to $15 would cost 1.4 million jobs, CBO says"

It's not hard to see, for anyone who can follow a logical train of thought:

In the 2019 estimate, the agency said total family income would decrease slightly on net.

“Higher wages would increase the cost to employers of producing goods and services,” the report said. “Employers would pass some of those increased costs on to consumers in the form of higher prices, and those higher prices, in turn, would lead consumers to purchase fewer goods and services. Employers would consequently produce fewer goods and services, and as a result, they would tend to reduce their employment of workers at all wage levels.”

Minimum wage pressure was just one of nine distinct pieces of evidence that I cited two weeks ago about the presence and imminent prospect of accelerating inflation. In summary form, the evidence for inflation already having arrived seemed to me fairly overwhelming:

an investment bank preparing for it

realtors and homebuyers (and sellers) seeing it very starkly

worker shortages and hiring desperation pay raises of 25% even when not compelled by law

surveyed consumers expecting it (and inflation has a built-in self-fulfilling-prophesy mechanism)

the Philly Fed seeing ample evidence of it in manufacturing

IHS Markit's PMI finding "inflationary pressures intensified" in both input prices and selling prices

shipping costs rising per CNBC

gasoline and crude oil prices up worldwide

minimum wage law boosted in some states and threatened to go national

Another major reason why I expect higher inflation is because the Fed wants there to be higher inflation. They have been very public that they want inflation to average 2% over a multi-year period. Since inflation has been consistently below 2% and closer to 1% in recent years, they are ready to tolerate inflation of around 3% for a while before deciding it's too much and time to do something about it. This is so well known by people who follow the Fed's pronouncements that I'm not going to spend any time finding a quotation to document it; readers can easily do that for themselves. Google "Powell inflation."

Notice from that NY Fed Survey of Consumer Expectations, above, that "Median inflation expectations at the one-year and three-year horizons remained unchanged at 3.0%." On the dot at three-point-zero. Maybe consumers are paying more attention to the news than I usually give them credit for.

For #11 and #12 on my list of inflationary factors or indications, I could add these two links for your consideration. The first of them concerns the steepness of the yield curve. That's at least one step more technical than the average high school grad is familiar with, so maybe some day I'll add further explanation, but today is not that day. The last link regards gold as an inflation hedge.

https://www.cnbc.com/2021/02/08/gold-markets-us-jobs-data-dollar.html

There's a lot of talk of inflation out there, pretty much everywhere I look, and even when I'm not looking for it. The latest such occurrence came when I just opened my weekly email newsletter from investing guru John Mauldin. He writes and quotes at considerable length, giving both sides of the fear-inflation and fear-not-inflation story. When I've mentioned Mauldin before, it's in the context of him being a pessimist about the post-COVID recovery. He still leans that way even as—as we've just seen this week, above—the CBO, the forecasters surveyed by the Philly-delphia Fed, and others that I've mentioned in previous weeks continue to break more and more positive with each new reading. But what he writes about the case for inflation fears is worth excerpting here [emphasis added], especially in regard to the full-sized $1.9tr Biden COVID bill that I wrote about last week.

Coming on top of trillions already authorized in prior bills, a budget deficit that was already approaching $2 trillion before the pandemic, and the Federal Reserve stimulating in its own ways, people are asking whether this is too much. The answer depends on the coronavirus “Gripping Hand.” If the vaccines work well enough, and are administered widely enough, to stop the new variants and enable economic normalcy later this year, all that money might be excessive. Rising consumer demand combined with supply constraints could spark inflation. …

The concern we may overstimulate took off this month when former Treasury Secretary Larry Summers, a Democrat, pointed out that it will far exceed the “output gap” shown in the latest Congressional Budget Office economic projections.

What is an output gap? Gross Domestic Product measures (or at least tries to) economic growth. Economists also calculate “potential GDP,” which is how much the economy could grow, if every available worker and other resource were fully employed.

Inflation tends to occur when actual GDP exceeds potential GDP because the economy is “running hot.” An output gap is when it goes the other way, with the economy operating well below its potential. That’s what we see in recessions.

Of course, all this involves numerous assumptions. GDP itself has problems, too, but it’s still a useful framework for analysis. Government and central bank policy should aim to keep the economy running roughly in line with its potential: not too hot, not too cold.

Larry Summers noted the Biden relief package will inject around $150 billion per month, while CBO says the monthly gap between actual and potential GDP is now around $50 billion, and will decline to $20 billion a month by year-end (because it assumes the COVID-19 virus and all its variants will be under control).

If correct, that would mean (at least to Summers and former Senator Phil Gramm, who wrote almost simultaneously a similar editorial for The Wall Street Journal) we are about to inject far more money than the economy can handle. It will have to emerge somewhere and may do so as price inflation. Here’s Summers:

[W]hile there are enormous uncertainties, there is a chance that macroeconomic stimulus on a scale closer to World War II levels than normal recession levels will set off inflationary pressures of a kind we have not seen in a generation, with consequences for the value of the dollar and financial stability. This will be manageable if monetary and fiscal policy can be rapidly adjusted to address the problem.

But given the commitments the Fed has made, administration officials’ dismissal of even the possibility of inflation, and the difficulties in mobilizing congressional support for tax increases or spending cuts, there is the risk of inflation expectations rising sharply. Stimulus measures of the magnitude contemplated are steps into the unknown.

Mauldin adds a list of 5 and then another 4 "reasons to worry about U.S. inflation," written by a former Federal Reserve Vice Chairman, some of which go beyond the dozen reasons that I've enumerated above.

I close with this link:

It's a fascinating animation of insured unemployment rate, state by state. Beware: once you start, you might have trouble stopping your viewing of this. Don't miss the quantum drop overall in national unemployment, even as you watch states move in and out and up and down in the worst 10 list.

Next week I'll finally publish my thoughts about Gamestop stock trading. Remember that? It was still on a lot of minds just one week ago, even if it seems like much longer. My contribution is so overdue as to be obsolete, but I have it all prepared, so I'll post it next week when maybe I'll have less to say about other topics.